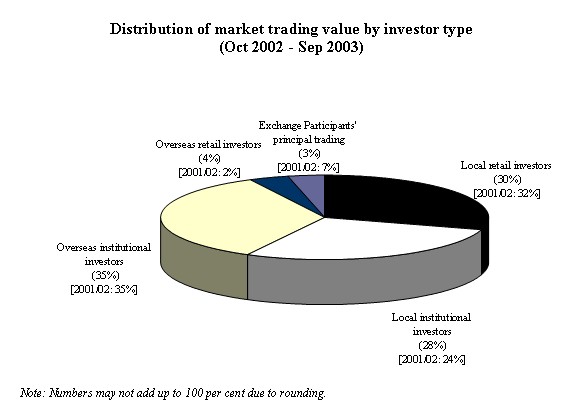

A recent survey by Hong Kong Exchanges and Clearing Limited (HKEx) shows that overseas institutional investors surpassed local retail investors for the third year in a row to be the largest investor group by turnover value in the HKEx securities market. There was also an increase in the contribution from local institutional investors for the third consecutive year.

The Cash Market Transaction Survey 2002/03 reveals that for the period from October 2002 to September 2003 local investors contributed 58 per cent of total market turnover value, while overseas investors, mainly institutional investors, contributed 39 per cent. The remaining 3 per cent was from Stock Exchange Participants' (EPs) principal trading (trading on the firm's own account). Local retail investors contributed 30 per cent of total market turnover value (down from 32 per cent the previous year) and local institutional investors contributed 28 per cent (up from 24 per cent in 2001/02 and 20 per cent in 2000/01). Overseas institutional investors contributed 35 per cent of total market turnover value and overseas retail investors 4 per cent.

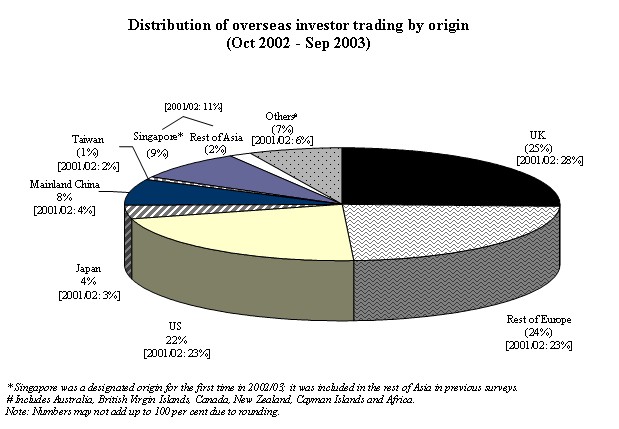

United Kingdom investors remained the largest overseas group, contributing 25 per cent of overseas investor trading (down from 28 per cent in 2001/02), followed by the rest of Europe (24 per cent, compared with 23 per cent in 2001/02) and the United States (22 per cent, compared with 23 per cent in 2001/02). Asia contributed 22 per cent of overseas investor trading, up from 20 per cent the previous year. Singapore and Mainland China were the Asian leaders, contributing 9 per cent and 8 per cent of overseas investor trading respectively. The contribution from Mainland China doubled to 8 per cent of overseas investor trading from 4 per cent in 2001/02.*

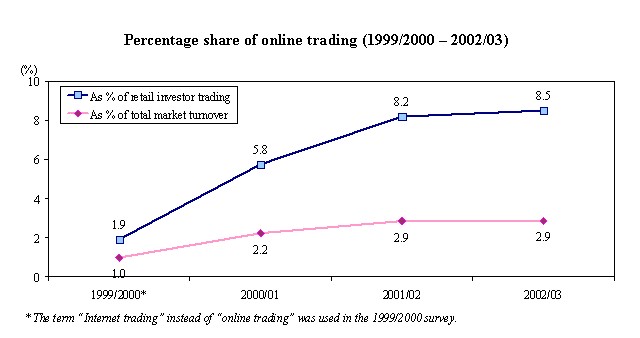

Online trading accounted for 8.5 per cent of retail investor trading or 2.9 per cent of total market turnover in 2002/03. The level of online trading was similar in 2001/02.

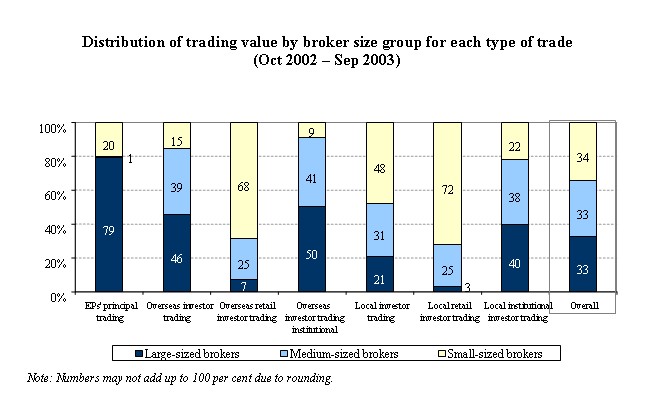

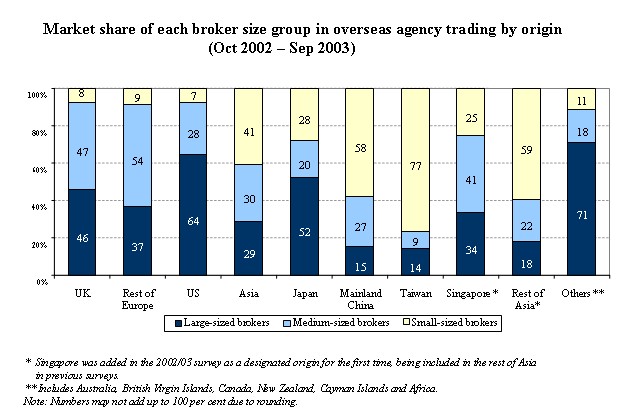

In the survey, EPs in the target population were divided into three groups with equal shares by turnover value -- eight large-sized brokers , 20 medium-sized brokers and 404 small-sized brokers. Almost half of local investor trading (48 per cent) was handled by small-sized brokers, while overseas investor trading was mainly channelled through large- and medium-sized brokers (46 per cent and 39 per cent respectively). Trading from the United Kingdom was channelled mainly through medium-sized brokers (47 per cent) and large-sized brokers (46 per cent); the majority of trading from the rest of Europe (54 per cent) was channelled through medium-sized brokers; and the majority of trading from the United States (64 per cent) was channelled through large-sized brokers. Small-sized brokers had the largest market share (41 per cent) in handling overseas investor trading from the Asian region.

The annual Cash Market Transaction Survey has been conducted since 1991. For the 2002/03 survey, questionnaires were sent to a target sample which included all large- and medium-sized brokers and a random sample covering 60 per cent of small-sized brokers in the target population. Out of the 290 questionnaires sent, 272 completed questionnaires were received. The response rate was 94 per cent by number or 98 per cent by turnover value of respondents. The findings are projected from the implied percentage shares of the different types of trade in the target population.

The full report on theCash Market Transaction Survey 2002/03is available on the HKEx website at: http://www.hkex.com.hk/eng/stat/research/research.htm.

* The survey's target respondents were EPs. Their responses stemmed from their own understanding of the origins of their clients. HKEx had no direct access to these clients, nor could it verify their identities.

One of the limitations of the survey is that EPs might not know the true origins of all their client orders. For instance, an EP might classify transactions for a local institution as such when in fact the orders originated from overseas and were placed through that local institution, or vice versa. As a result, the findings may deviate somewhat from the true picture.