Hong Kong Exchanges and Clearing Limited’s (HKEx) Derivatives Market Transaction Survey 2009/10 (covering the period from July 2009 to June 2010) found that the contribution of overseas investors (primarily institutions) to the trading in HKEx’s derivatives (futures and options) market reached the highest level in the recent five years. This made the three-pillar support for derivatives trading stronger — half by Exchange Participants’ (EPs) principal trading and the other half equally supported by local investors (primarily individuals) and overseas investors.

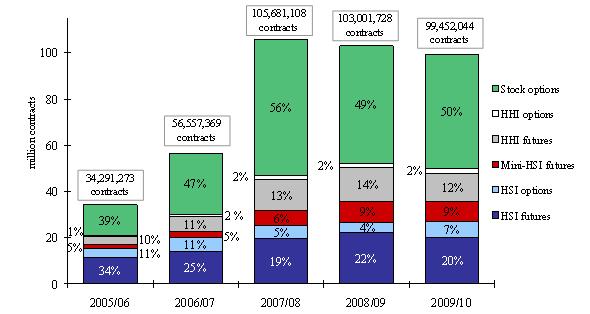

In 2009/10, the turnover for the futures and options under study was 99 million contracts (referred to as the total market turnover in this survey), down 4 per cent from 103 million contracts in 2008/09. Stock options remained the dominant product by turnover, contributing half of the total market turnover (as measured by contract volume) (see Figure 1).

Some key findings of the 2009/10 survey

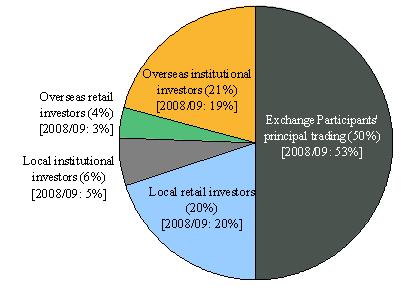

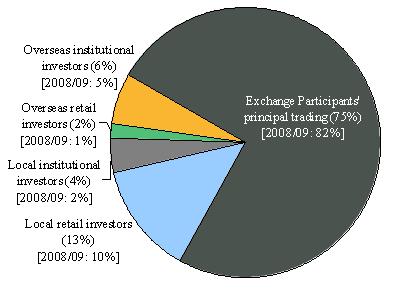

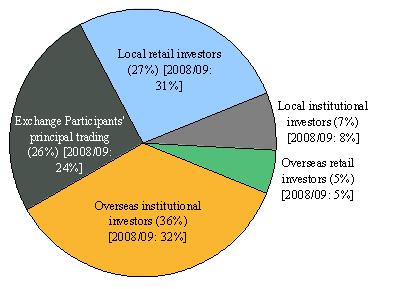

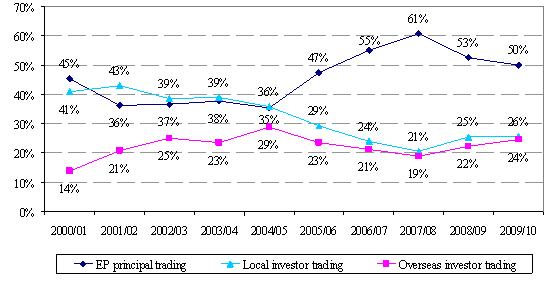

- EP principal trading (comprising market maker trading and EP proprietary trading) contributed 50 per cent of total market turnover (down from 53 per cent in 2008/09), 75 per cent of stock options turnover (down from 82 per cent in 2008/09) and 26 per cent of turnover in other futures and options (compared to 24 per cent in 2008/09) (see Figure 2).

- Local investors contributed 26 per cent of total market turnover (compared to 25 per cent in 2008/09), and overseas investors contributed 24 per cent (up from 22 per cent in 2008/09) (see Figure 3).

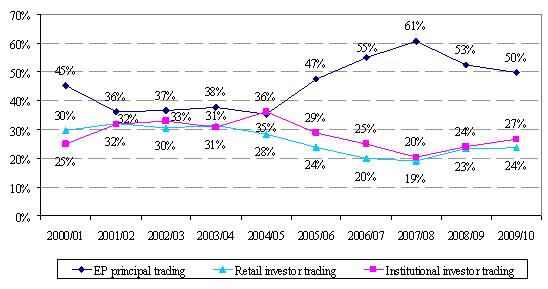

- Retail investors contributed 24 per cent of total market turnover (compared to 23 per cent in 2008/09), mostly from local retail investors (20 per cent). Institutional investors contributed 27 per cent in 2009/10 (up from 24 per cent in 2008/09), mostly from overseas institutional investors (21 per cent) (see Figures 2 and 3).

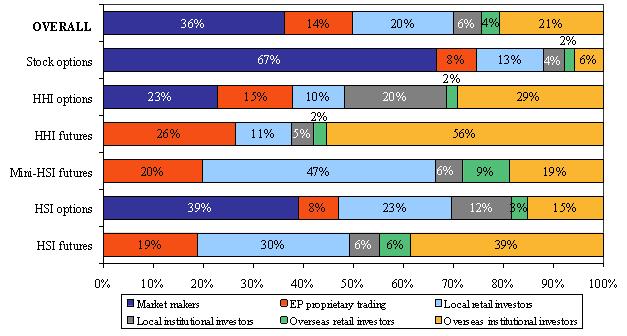

- Major products (see Figure 4):

- For Hang Seng Index (HSI) futures, overseas institutional and local retail investors were the major contributors (39 per cent and 30 per cent respectively of the product’s turnover).

- For Mini-HSI futures, the major contributor was local retail investors (47 per cent) while overseas investors’ contribution was also significant (28 per cent, 19 per cent from institutions).

- For H-shares Index (HHI) futures, overseas investors were the major contributors (58 per cent: 56 per cent from institutions, 2 per cent from individuals).

- For HHI options, EP principal trading and overseas institutional investors were the major contributors (38 per cent and 29 per cent respectively).

- For stock options and HSI options, EP principal trading was dominant (75 per cent and 47 per cent respectively).

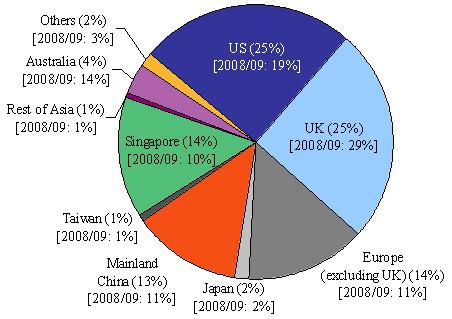

- Among overseas investors, UK investors and US investors were the two largest groups in 2009/10, both contributing 25 per cent of total overseas investor trading. However, UK investors’ contribution dropped from 29 per cent in 2008/09 while US investors’ contribution grew from 19 per cent in 2008/09. The contributions from European (excluding UK), Singaporean and Mainland China investors were also significant (13-14 per cent in 2009/10, compared to 10-11 per cent in 2008/09). Mainland investors contributed 13 per cent of overseas investor trading and 43 per cent of the trading from Asia, excluding Hong Kong. (See Figure 5).

- Retail online trading contributed 51 per cent of total retail investor trading (43 per cent in 2008/09) and 12 per cent to total market turnover (10 per cent in 2008/09) (see Figure 6).

The Derivatives Market Transaction Survey has been conducted annually along similar lines since 1994. The surveys for the latest five years covered HSI futures, HSI options, Mini-HSI futures, HHI futures, HHI options and stock options. These products together accounted for 98.6 per cent of the total turnover of the HKEx derivatives market during the study period of the 2009/10 survey. The survey had an overall response rate of 90 per cent and the respondents contributed 99 per cent of the total turnover in products under study during the study period.

The full report on the HKEx Derivatives Market Transaction Survey 2009/10 is available on the HKEx website at:http://www.hkex.com.hk/eng/stat/research/Documents/DMTS10.pdf.

Notes:

- “Market turnover” in the report refers to the total turnover, measured in contracts traded, of the products under study.

- Due to their dominance by contract volume, stock options have a large influence on the trading pattern of the HKEx derivatives market even though they have much smaller notional value than the other futures and options.

- HKEx surveyed Exchange Participants only. Their responses stemmed from their own understanding of their clients. HKEx had no direct access to these clients, nor could it verify their nature.

- The survey is subject to a number of limitations. For example, an Exchange Participant might not know the true origins of all its client orders. The Exchange Participant might classify transactions for a local institution as such when in fact the orders originated overseas and were placed through that local institution, or vice versa. As a result, the findings may deviate somewhat from the true picture.

Figure 1. Contract volume and percentage of total by product under study

(2005/06 – 2009/10)

Note: Numbers may not add up to 100 per cent due to rounding.

Figure 2. Distribution of derivatives market trading volume by investor type

(Jul 2009 – Jun 2010)

(a) Overall

(b) Stock options

(c) Futures & options (excluding stock options)

| Notes: |

(1) |

Exchange Participants' principal trading comprised market maker trading and EP proprietary trading. |

|

(2) |

Numbers may not add up to 100 per cent due to rounding. |

Figure 3. Distribution of derivatives market trading volume by investor type

(2000/01 – 2009/10)

(a) Local vs overseas

(b) Retail vs institutional

Note: Numbers may not add up to 100 per cent due to rounding.

Figure 4. Distribution of derivatives market trading volume by investor type

for overall market and each product (Jul 2009 – Jun 2010)

| Notes: |

(1) |

Market maker trading and EP proprietary trading are components of EP principal trading. |

|

(2) |

Numbers may not add up to 100 per cent due to rounding. |

Figure 5. Distribution of overseas investor trading volume in derivatives by origin

(Jul 2009 – Jun 2010)

|

*

|

Reported origins in “Others” in 2009/2010 comprisedAfrica,Belize,British Virgin Islands,Canada,Caribbean,Cayman Islands,Liberia,Middle EastandNew Zealand.

|

|

Note:

|

Numbers may not add up to 100 per cent due to rounding.

|

Figure 6. Retail online trading to total derivatives market volume

and retail turnover volume (2001/02 – 2009/10)

|

Note:

|

Figures before 2009/10 for the percentage of online trading to total market volume/total retail turnover volume were adjusted to reflect refinement in the calculation of total implied online trading volume for the overall market.

|

Ends