- Exchange proposes to tighten the reverse takeover (RTO) Rules and continuing listing criteria to address concerns about backdoor listings and shell activities

- Proposed Rule changes are targeted at shell activities and aim to maintain a quality market; they are not intended to restrict legitimate business expansion or diversification by listed issuers

- Exchange also published a guidance letter on listed issuer’s suitability for continued listing

The Stock Exchange of Hong Kong Limited (the Exchange), a wholly owned subsidiary of Hong Kong Exchanges and Clearing Limited (HKEX), today (Friday) published (i) the consultation paper on backdoor listing, continuing listing criteria and other Rule amendments; and (ii) the guidance letter on listed issuer’s suitability for continued listing (GL96-18).

The consultation paper seeks market views on proposed changes to the Listing Rules to address concerns over backdoor listings and “shell” activities. This forms part of the Exchange’s ongoing holistic review of its Rules to tackle problematic corporate behaviour with a view to maintaining the quality and reputation of the Hong Kong market.

In recent years, the Exchange has noted an increase in market activities related to the trading of, and the creation of “shell companies”. These activities are driven by the demand for “shell companies” for backdoor listings. To maintain a quality market, the Exchange has taken a robust approach in applying the Rules to address evolving backdoor listing structures, corporate actions to strip out operations from listed issuers, and issuers conducting very low levels of operations. The Exchange has published guidance materials in these areas.

“The Exchange is applying a three-pronged approach in curbing shell activities: first, tightening its suitability review of new applicants to address concerns on shell creation through IPOs; second, enhancing the continuing listing criteria for listed issuers to deter the manufacturing and maintenance of listed shells; and third, tightening the RTO Rules to prevent backdoor listings particularly those involving shell companies,” said David Graham, HKEX Head of Listing. “While shell activities are limited to a small segment of our market, they undermine investors’ confidence and overall market quality. At this point there is a need to formalise our guidance into the Rules, and to make Rule amendments to address some issues in a more effective manner.”

“Our proposals are targeted at shell activities and seek to address specific identified issues. They are not intended to restrict listed issuers from legitimate business expansion or diversification that are part of the issuers’ business strategies,” Mr Graham added. “We are mindful of the impact of the proposed changes to the continuing listing criteria on a limited number of issuers. Under the proposals, there will be a transitional period of 12 months for those issuers to take corporate actions to comply with the Rules as amended. We will provide some flexibility when considering the application of the new RTO Rules to these proposed actions, with a view to facilitating issuers’ compliance with the new Rules on continuing listing obligations.”

A summary of the proposed Rule amendments is set out in the Attachment.

The Exchange has also issued guidance letter GL96-18 on listed issuer’s suitability for continued listing (effective today), citing examples of circumstances where the Exchange may raise concerns whether a listed issuer or its business continues to be suitable for listing. As an example, the Exchange may question an issuer’s suitability for listing if it has concerns that the issuer may be carrying on its business for the purpose of maintaining a listing status, rather than genuinely operating a business of substance.

“In addition, we are conducting a review on the specific requirements applicable to listed issuers publishing audited financial statements with disclaimer or adverse audit opinions,” Mr Graham said. “We are developing proposed Rule amendments in this area to enhance the quality and reliability of financial information and any such amendments will include an appropriate transitional period for those issuers to remedy the audit issues and comply with the new Rules. We plan to publish a consultation paper later this year to seek market views.”

The Consultation Paper and Questionnaires on Backdoor Listing, Continuing Listing Criteria and other Rule amendments and the Guidance Letter on Listed Issuer’s Suitability for Continued Listing can be downloaded from the HKEX website.

The Exchange invites market feedback on the proposals contained in the consultation paper. The deadline for responses is 31 August 2018.

Attachment – Summary of proposals

| I. |

Proposals relating to backdoor listing

The proposals formalise the Exchange’s practices in regulating backdoor listings, and impose additional requirements to address specific issues and backdoor transaction structures, including concerns about new investors acquiring de facto control of an issuer and subsequently using it as a listing platform to acquire new businesses and circumvent the new listing requirements, or issuers breaking up acquisitions into a series of small acquisitions, or acquiring a new business that does not meet new listing requirements and subsequently, disposing its original businesses.

|

| |

(a) |

Definition of an RTO transaction

|

| |

|

1. |

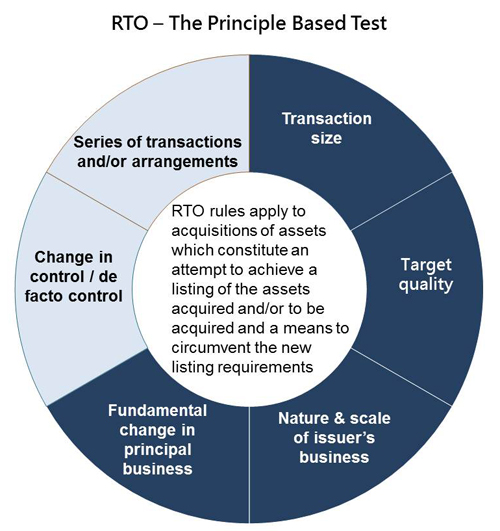

RTO – Principle based test |

| |

|

|

- Codify the principle based test (set out in Guidance Letter GL78-14) with modifications to two assessment criteria:

|

| |

|

|

| Change in control / de facto control

Indicative factors of a change in de facto control: (i) substantial change in board / key management; (ii) change in single largest substantial shareholder, and (iii) issue of restricted convertible securities.

|

|

|

Series of transactions and/or arrangements

Include transactions and/or arrangements that are in reasonable proximity (normally within 36 months) or are otherwise related, and may include changes in control/ de facto control, acquisitions, disposals or termination of the original businesses, and in some circumstances, greenfield operations or equity fundraisings related to acquisitions of new lines of businesses.

The entire series of transactions and/or arrangements would be treated as if it were one transaction (consequently, a disposal may trigger an RTO ruling on a previously completed acquisition in the same series, or a number of smaller acquisitions may form an RTO). |

|

| |

|

2. |

RTO – Bright line tests |

| |

|

|

- Retain and modify the bright line tests:

- RTO rules apply to very substantial acquisition(s) from the controlling shareholder within 36 months from a change in control (as defined under the Takeovers Code).

- Disposal restriction applies to restrict any material disposal at the time of or within 36 months after a change in control of the issuer (as defined under the Takeovers Code), unless the remaining business, or any assets acquired after the change in control, can meet Rule 8.05.The Exchange may also apply this disposal restriction to a material disposal proposed at the time of or within 36 months after a change in the single largest substantial shareholder of the issuer.

|

| |

|

3. |

Backdoor listings through large scale issue of securities |

| |

|

|

- Codify Guidance Letter GL84-15 into the Rules to disallow backdoor listings through large scale issue of securities for cash, where the proceeds will be applied to acquire and/or develop new business that is expected to be substantially larger than the issuer’s existing principal business.

|

| |

(b) |

Tighten the compliance requirements for RTOs and extreme transactions

The proposals aim to discourage the use of “shell” companies for backdoor listings and to ensure the acquisition targets that are the subject of new listing under the RTO Rules are suitable for listing.

|

| |

|

- The acquisition targets must be suitable for listing (Rule 8.04) and meet the trading record requirements for new applicants (Rule 8.05), and the enlarged group must meet all the new listing requirements (except Rule 8.05).For issuers that do not comply with Rule 13.24 (normally suspended companies), each of the acquisition targets and the enlarged group must comply with all the new listing requirements.

- Codify the “extreme VSAs” category set out in Guidance Letter GL78-14 and rename as “extreme transactions”. “Shell companies” are not eligible for this category and accordingly, the issuer must either i) operate a principal business of substantial size; or

ii) have been under the long-term control of a large business enterprise and the acquisition forms part of a business restructuring with no change in control.

- Where an RTO or an extreme transaction involves a series of transactions and/or arrangements, issuers are required to include in the listing document or circular the pro forma income statement of all acquisition targets and any new business developed that are part of the series.

|

| II. |

Proposals relating to continuing listing criteria

The proposed amendments to the continuing listing criteria aim to address specific concerns about some issuers that attempt to maintain the listing status by holding significant assets or investments, rather than operating businesses that have substance and are viable and sustainable in the longer term:

|

| |

(a) |

Amend Rule 13.24 (sufficiency of operations) |

| |

|

- Requires a listed issuer to carry out a business with a sufficient level of operations and assets of sufficient value to warrant its continued listing (and not sufficient operations or assets set out in the current Rule). This excludes any securities trading and/or investment activities (other than a Chapter 21 investment company). A listed issuer would not meet this Rule if it does not operate a business that has substance and/or is viable and sustainable.

|

| |

(b) |

Amend Rules 14.82 and 14.83 (cash companies) |

| |

|

- Amend the definition of “short-dated securities” in the cash company Rules to include investments that are easily convertible into cash (eg investments in listed securities).The exemption for securities brokerage companies will only apply to clients’ assets.

|

| |

(c) |

Proposed transitional arrangements |

| |

|

- A 12-month transitional period applies for issuers not meeting the continuing listing criteria as amended.No transitional period for the proposed amendments to the RTO Rules, however, if issuers conduct transactions with a view to re-comply with the new Rules, the Exchange would take this into account with the objective of facilitating their re-compliance.

|

| III. |

Other proposed Rule amendments

The Exchange also proposes to enhance the Rule requirements in the following areas:

|

| |

- Securities transactions:

- confine the revenue exemption from the notifiable transaction requirements to purchases and sales of securities only if they are conducted by members of the issuer group that are subject to the supervision of prudential regulators (ie banking companies, insurance companies, or securities houses); and

- add a specific requirement for issuers to disclose in their annual reports details of each securities investment that represents 5 per cent or more of their total assets;

- Significant distribution in specie of unlisted assets

- codify Listing Decision LD75-4 to impose additional requirements on distribution in specie that is equivalent in size to a very substantial disposal, comparable to requirements for a withdrawal of listing;

- Other matters relating to notifiable or connected transactions

- require (i) disclosure on the outcome of any guarantee on the financial performance of an acquisition target that is subject to the notifiable or connected transaction requirements (irrespective of whether the guaranteed financial performance is met) in the next annual report; and (ii) disclosure by way of an announcement if (a) there is any subsequent change to the guarantee; or (b) the actual financial performance of the target acquired fails to meet the guarantee (currently required for a connected transaction only);

- require (i) disclosure on the identities of the parties to a transaction in the announcements of notifiable transactions; and (ii) disclosure on the identities and activities of the parties to the transaction and of their ultimate beneficial owners in the announcements of connected transactions; and

- amend the Rules to make it clear that where any calculation of the percentage ratios produces an anomalous result or is inappropriate to the sphere of activity of the listed issuer, the Exchange (or the issuer) may apply an alternative size test that it considers appropriate to assess the materiality of a transaction under Chapter 14 or 14A.

|

Ends