Hong Kong Exchanges and Clearing Limited (HKEx)’s derivatives market, which comprises a variety of futures and options contracts, gets equal support from Exchange Participants and investors, according to the Derivatives Market Transaction Survey 2005/06.

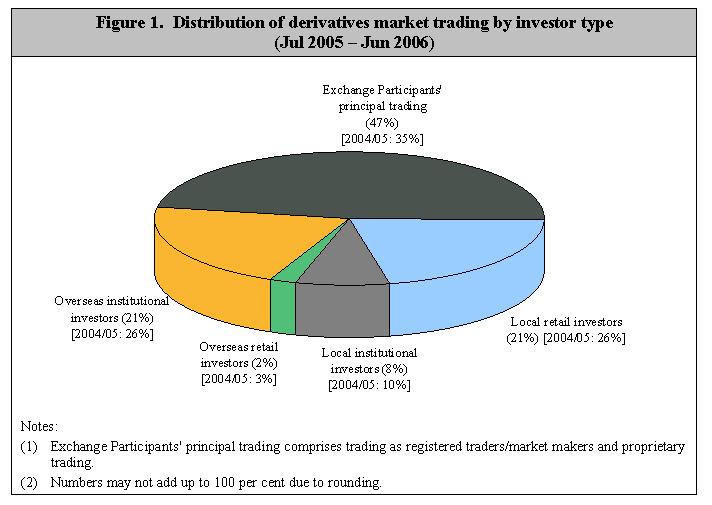

Overall, Exchange Participants’ principal trading contributed 47 per cent to total derivatives contract volume (vs 35 per cent in 2004/05), retail investors 24 per cent (vs 28 per cent in 2004/05) and institutional investors 29 per cent (vs 36 per cent in 2004/05), the survey revealed. Retail investors participating in the derivatives market were mainly local investors while institutional investors were mainly from overseas (both contributed 21 per cent of total derivatives volume). Overseas retail investors contributed only 2 per cent of total volume and local institutional investors 8 per cent.

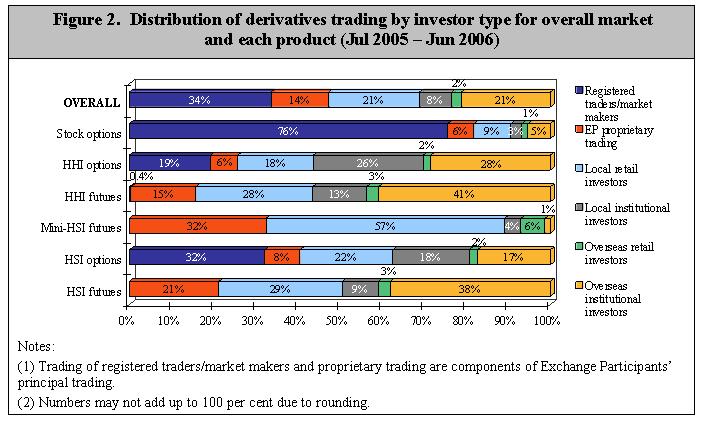

Different products attracted a different investor mix. For stock options, the majority of turnover was Exchange Participants’ principal trading, which accounted for 82 per cent (76 per cent from market making) of the product’s total volume in 2005/06. Overseas institutional investors were the major contributors to trading in Hang Seng Index (HSI) Futures (38 per cent) and H-shares Index (HHI) Futures (41 per cent). For Mini-HSI Futures, local retail investors continued to be the dominant participants (contributing 57 per cent of product turnover). For HHI Options, the contributions from overseas and local institutional investors (28 per cent and 26 per cent respectively) and Exchange Participants’ principal trading (26 per cent) were equally significant. The majority of turnover in HSI Options was Exchange Participants’ principal trading (41 per cent).

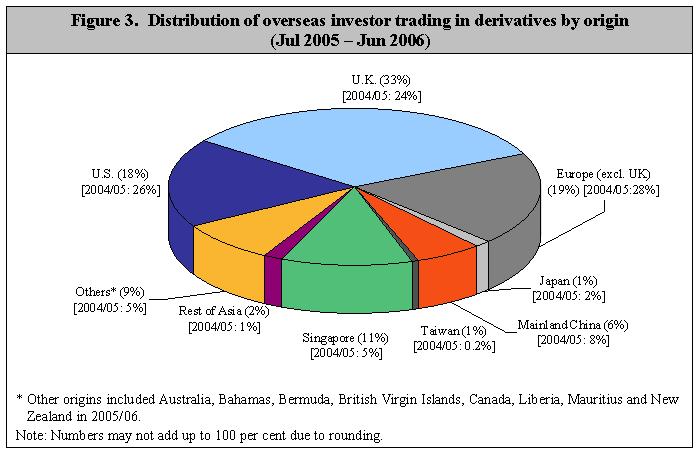

The contribution from overseas investors (mainly institutions) was 23 per cent in 2005/06 (vs 29 per cent in 2004/05). Among overseas investors, the largest contributors were investors from the UK, with 33 per cent of overseas investor trading in 2005/06. They were followed by investors from Europe (excluding the UK) and the US, who contributed 19 per cent and 18 per cent of overseas investor trading respectively.

Pure trading remained the main driver of derivatives market transactions, accounting for 49 per cent of the total market turnover in 2005/06 (vs 50 per cent in 2004/05). The proportion of turnover for hedging was 32 per cent (vs 36 per cent in 2004/05), and the remaining 19 per cent was turnover for arbitrage (vs 14 per cent in 2004/05).

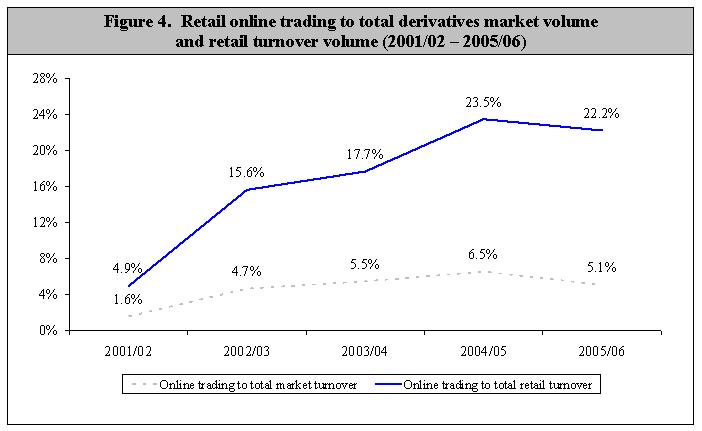

Retail online trading contributed 22.2 per cent of total retail investor trading in 2005/06, compared to 23.5 per cent in 2004/05. Its contribution to total market turnover was 5.1 per cent, compared to 6.5 per cent in 2004/05.

The Derivatives Market Transaction Survey has been conducted annually along similar lines since 1994. This year’s survey covered HSI Futures, HSI Options, Mini-HSI Futures, HHI Futures, HHI Options (introduced on 14 June 2004 and covered in the survey for the first time) and stock options, which together accounted for about 99.7 per cent of the total turnover of the HKEx derivatives market during the study period (July 2005 to June 2006). The survey had an overall response rate of 85 per cent and the respondents contributed 96 per cent of the total turnover during the study period.

The full report on the HKEx Derivatives Market Transaction Survey 2005/06 is available on the HKEx website at:http://www.hkex.com.hk/eng/stat/research/research.htm.

| 2. |

HKEx surveyed Exchange Participants only. Their responses stemmed from their own understanding of their clients. HKEx had no direct access to these clients, nor could it verify their identities.

|

| 3. |

One of the limitations of the survey is that Exchange Participants might not know the true origins of all their client orders. For instance, an Exchange Participant might classify transactions for a local institution as such when in fact the orders originated from overseas and were placed through that local institution, or vice versa. As a result, the findings may deviate somewhat from the true picture.

|