A survey conducted by Hong Kong Exchanges and Clearing Limited (HKEx) during the period from 16 November 2007 to 15 January 20081 revealed that one in three adults in Hong Kong are stock investors (individuals invested in the HKEx stock market). Retail investors, ie individuals who participate in the stock or derivatives (ie futures and options) markets of HKEx or both, have risen to 35.8 per cent of the adult population, up from 28.8 per cent in 2005, according to the survey.

The Retail Investor Survey 2007 revealed that:

|

|

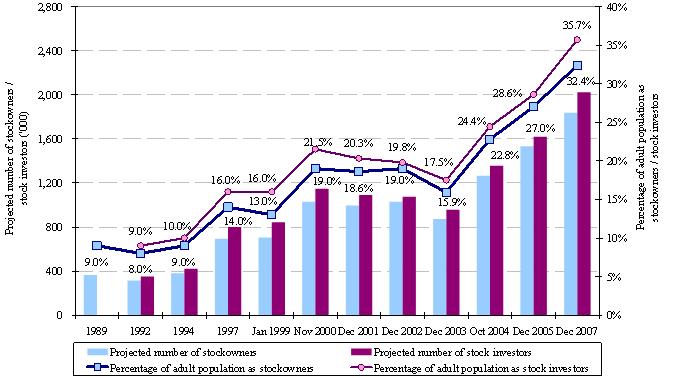

32.4 per cent of Hong Kong adults were stockowners who were holding stocks at the time of interview. The median stockholding value was $100,000.

|

|

|

About 20 per cent of stock investors (or 7 per cent of the adult population) invested in warrants2 (ie were holding warrants at the time of interview or had traded them in the 12-month period preceding the interview).

|

|

|

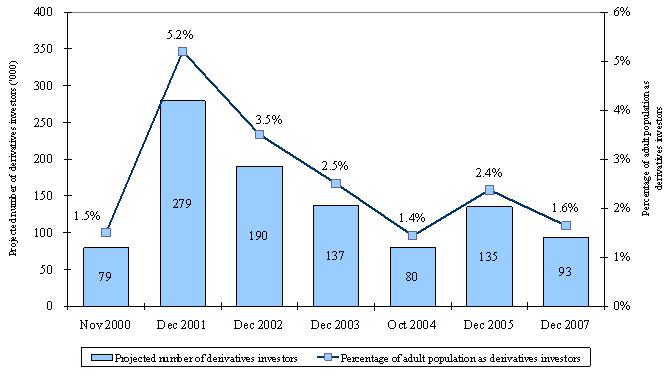

1.6 per cent of Hong Kong adults (or 93,000 individuals) were derivatives investors (individuals who at the time of the interview were holding futures or options traded on the HKEx derivatives market or had traded them in the 12-month period preceding the interview).3

|

|

|

Collectively, 35.8 per cent of Hong Kong adults (or 2,024,000 individuals) were retail investors who were either stock investors or derivatives investors, or both.

|

|

|

Among stock investors, 85.7 per cent were stock traders (ie had traded stocks in the 12-month period preceding the interview).

|

|

|

58.8 per cent of stock traders were online stock traders who had traded stocks via online media during the 12-month period (up from 38.5 per cent in 2005) while 49.2 per cent of derivatives investors were online derivatives traders who had traded derivatives via online media during the 12-month period (up from 37.5 per cent in 2005).

|

|

|

62.9 per cent of stock traders had traded solely through banks (up from 59.1 per cent in 2005) and 22.6 per cent solely through broker firms (down from 30.8 per cent in 2005). About 48 per cent of derivatives traders had traded solely through broker firms (up from 41.2 per cent in 2005) and 36.7 per cent solely through banks (down from 48.5 per cent in 2005). |

The typical Hong Kong retail stock investor during the survey period was a 42 year-old, with upper secondary or above education, a monthly personal income of about $22,500 and a monthly household income of about $35,000.

The typical Hong Kong retail derivatives investor was a 42 year-old, with matriculation or above education, a monthly personal income of about $35,000 and a monthly household income of about $55,000.

Stock investors traded more frequently in 2007 than in 2005 — the median number of stock transactions during the 12-month period in 2007 was 10, up from five in 2005. For stock traders only (ie excluding those who had not traded), the median number of stock transactions was 15; the average value per stock transaction during the 12-month period for a stock trader had a median of $35,000. The median implied total stock transaction value per stock trader during the 12-month period was $500,0004, up from $340,000 in 2005.

Derivatives investors also traded more frequently in 2007 than in 2005 — the median number of derivatives transactions during the 12-month period in 2007 was 10, up from six in 20055. The average contract volume per derivatives transaction during the 12-month period for a derivatives investor had a median of two, compared to three in 2005. The median implied total contract volume per derivatives investor during the 12-month period was 40, higher than the 24 in 2005.6

Compared to non-online stock traders, online stock traders tended to be younger, with higher education level and higher work status. They also tended to have a higher stockholding value and to have traded more frequently.

Stock traders who traded mainly through broker firms tended to have a higher stockholding value, to have traded more frequently and with a higher deal size than those who traded mainly through banks.

Stock investors were generally positive about the various aspects of the Hong Kong stock market (all aspects had mean scores above 4 on a 7-point scale with 1 being strongly disagree and 7 being strongly agree). Derivatives investors were also generally positive about the various aspects of HKEx’s derivatives market (all aspects had mean scores close to 5). Retail investors were also positive when asked whether “HKEx gives priority to the public interest”.

The Retail Investor Survey has been conducted periodically since 1989. In the Retail Investor Survey 2007, 2,292 individuals were interviewed by telephone.

A full report of the Retail Investor Survey 2007 and reports on past surveys are available on the HKEx website at: http://www.hkex.com.hk/research/research.htm.

Attached are selected findings of the survey presented in tables and charts.

Figure 1. Trend of stockowners and stock investors

Figure 2. Trend of derivatives investors