Variation Margin reflects the daily change in market value of the contracts, i.e. the daily gain or loss of a contract due to market movements. On a daily basis, OTC Clear conducts a valuation of each contract (also known as “mark to market”) to calculate Variation Margin and monitors the valuation results regularly to assess the amount payable to and/or receivable by the Clearing Members for all cleared contracts.

Valuation methodologies used to evaluate the daily change in market value are transparent and well recognized by the industry. The market data used for valuation is obtained from reputable third party vendors, and is updated intra-day. OTC Clear will review the data to ensure its representativeness of current market conditions and the data will be made available to Clearing Members for daily reconciliation.

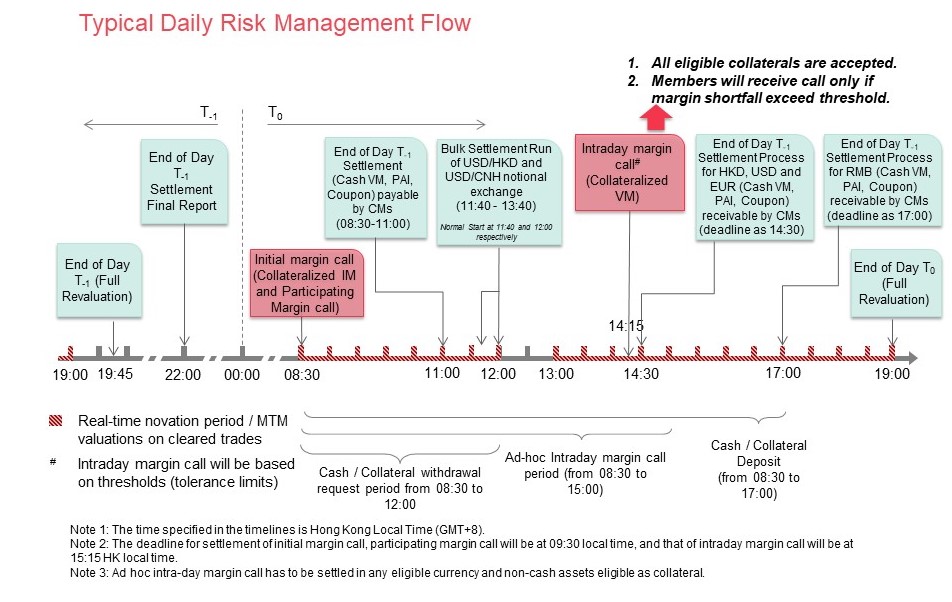

OTC Clear will issue margin calls to Clearing Members and will collect collateral to cover the current exposures of Clearing Members’ portfolios. Clearing Members are required to settle the margin calls demanded by OTC Clear within the timeframe stipulated in the Clearing Rules and Procedures. Currently, OTC Clear has the right to issue the following types of margin calls:

- Routine/Ad hoc Intra-day Margin Call;

- End of day Initial Margin Call;

- Participating Margin Call; and

- Other types of margin calls as described in the OTC Clear Rates and FX Derivatives Clearing Procedures.

The diagram below shows the timelines of margin calls and the daily risk management process. For details of margin calls, please refer to the OTC Clear Clearing Rules and Procedures.

Daily Risk Management / Settlement timelines